In China, conversations around aging are starting earlier and becoming more specific. It is increasingly common to see younger consumers paying attention to subtle skin changes, while older groups focus on maintaining overall condition rather than reversing it. At the same time, people are becoming more selective in what they use. Consumers are reading ingredient lists, comparing functions, and choosing products based on their own needs rather than general claims. What used to be a broad concern is now approached in a much more personal and targeted way.

Download the 2026 China Beauty Report here

Rapid growth and declining concentration signal expanding demand and diversified consumer needs of the Chinese anti-aging market

The global anti-aging market has maintained strong expansion, with a CAGR of 13.3% from 2015 to 2025. Compared to the global market, the Chinese anti-aging market is growing even faster, emerging as a key growth engine with a 16% CAGR over 2016–2025. The market is expected to exceed RMB 153.2 billion by 2026, indicating continued expansion in both market size and demand. This faster growth in China is largely driven by increasing consumer acceptance of anti-aging products and the earlier adoption of anti-aging routines, rather than simply following global trends.

Growth is driven by an expanding consumer base across age groups. On one hand, population aging is fueling the development of the “silver economy.” Their demand is shifting from basic healthcare to quality-of-life products such as skincare, supplements, and medical aesthetics. On the other hand, younger consumers are entering the category earlier. They are treating anti-aging as preventive care rather than something to address later. This is increasingly visible in the popularity of light medical aesthetics among young consumers, with some even traveling to Korea for short, weekend treatments. Together, this broadens the market and extends the consumption cycle.

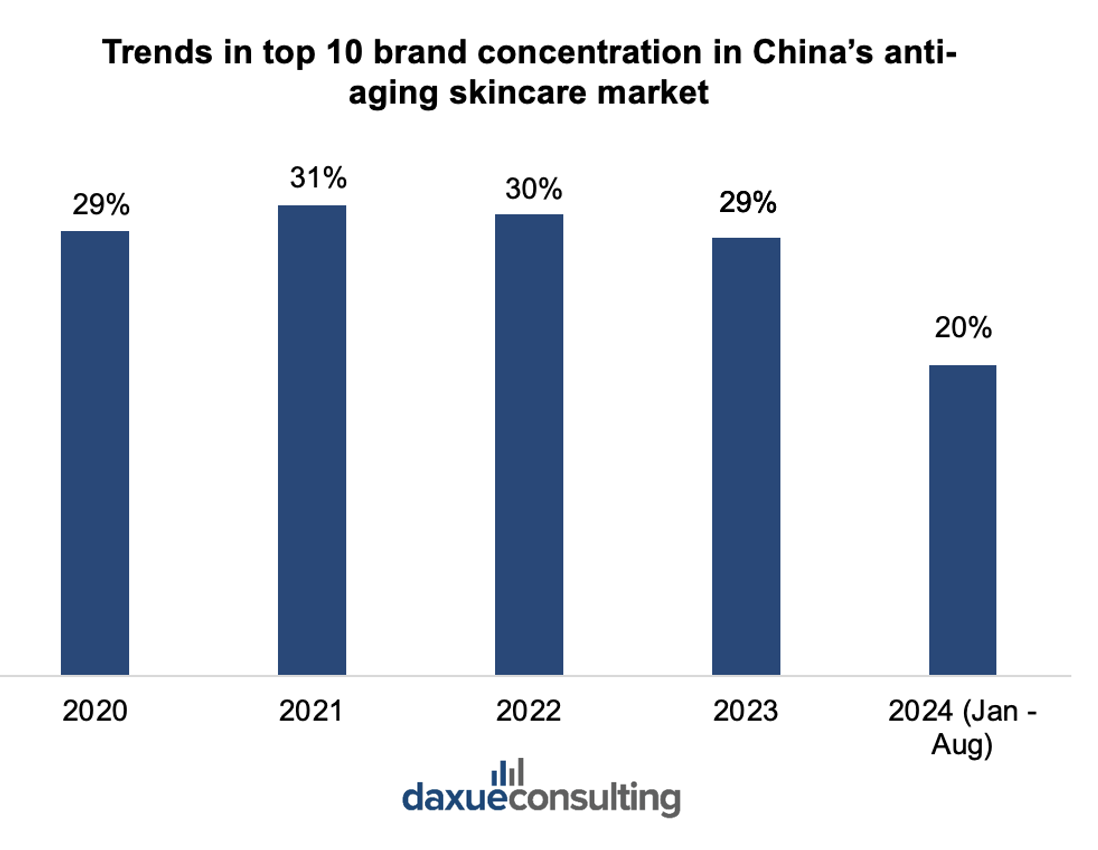

At the same time, market concentration has been declining, with CR10 (top 10 brands’ market share) falling from 30.8% to 20.3% since 2021. This suggests a more fragmented and competitive landscape, where new and foreign brands have more room to enter. It also reflects increasingly diverse consumer preferences, as demand shifts toward more targeted and differentiated products.

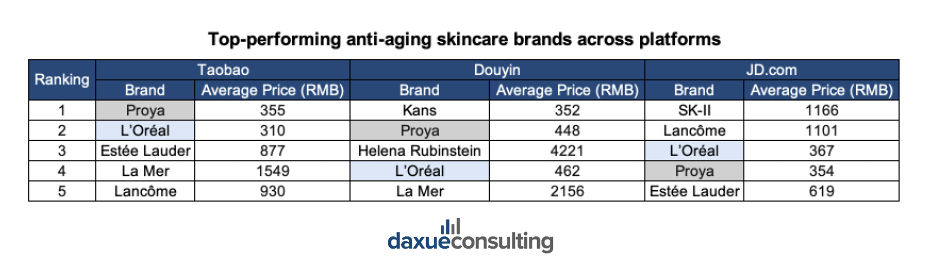

Proya and L’Oréal lead the fragmented anti-aging platform landscape

The distribution of top-performing anti-aging skincare brands across platforms reveals both consistency and clear positioning differences. Proya and L’Oréal stand out as the only brands that rank among the top players across all three platforms (Taobao, Douyin, and JD.com). This highlights their strong cross-channel presence and broad consumer appeal. On Taobao, the brand mix is relatively balanced, with both domestic and international brands competing across mid- to premium price ranges. Douyin, however, shows a wider price dispersion, with high-end brands such as Helena Rubinstein reaching significantly higher average prices, suggesting stronger premium storytelling and content-driven sales. In contrast, JD.com is more heavily skewed toward established international luxury brands like SK-II and Lancôme, with consistently higher average price points.

Diversified and increasingly specialized consumer needs are reshaping product demand in China’s anti-aging market

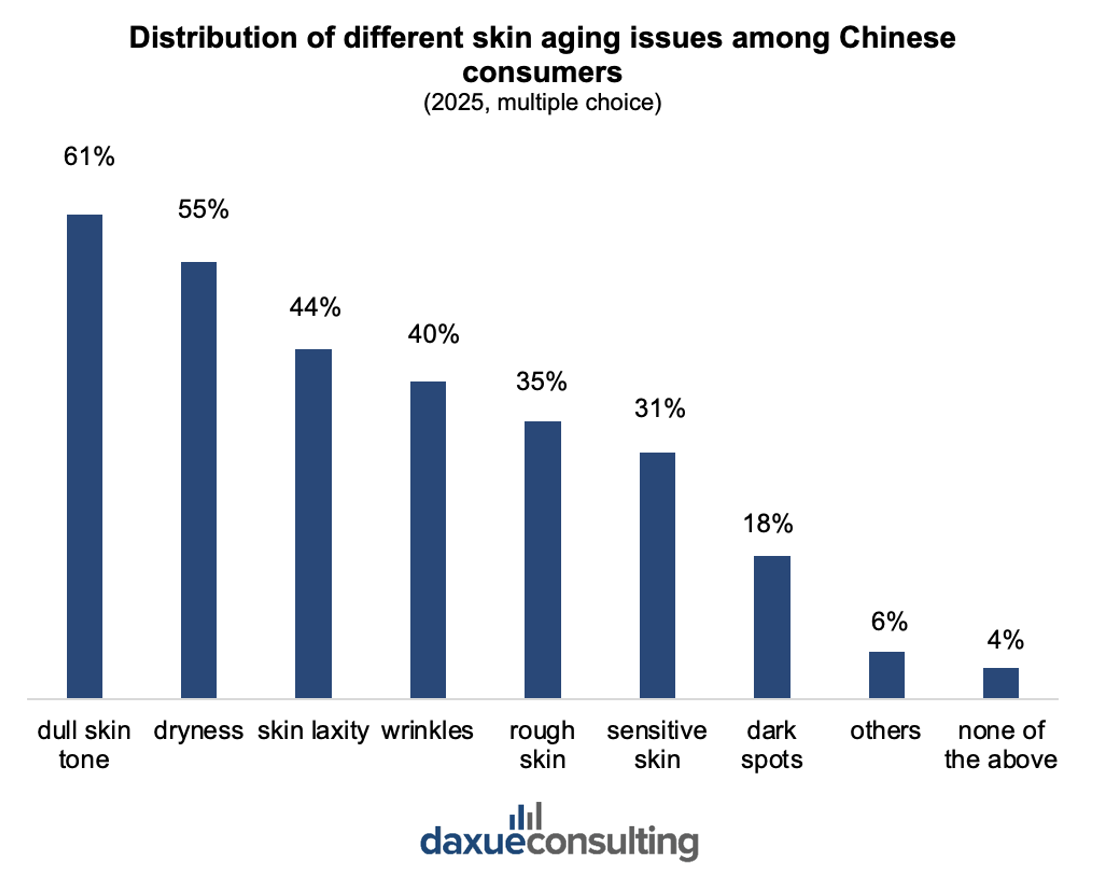

The decline in market concentration reflects a deeper structural shift: consumer demand is becoming increasingly fragmented and specialized. Rather than relying on broad, one-size-fits-all solutions, consumers are now seeking targeted products that address specific skin concerns. Survey data shows that 61.2% of consumers are concerned about dull skin tone, 55% about dryness, and 43.8% about skin laxity, indicating a clear move from generalized anti-aging toward more precise, function-driven solutions. This shift is pushing brands to move beyond generic “anti-aging” claims and develop more targeted product offerings.

Sensitive skin: A self-inflicted market gap

Within this trend, sensitive skin is emerging as an important opportunity segment. Around 31.2% of consumers identify as having sensitive skin, with 58.3% classified as mildly sensitive. Compared to the broader population, this group places greater emphasis not only on efficacy but also on safety, gentleness, and ingredient transparency. Part of this rise is not entirely natural. It is increasingly iatrogenic, driven by the overuse of active ingredients such as acids and early-stage retinol. While effective, these ingredients are known to disrupt the skin barrier and cause irritation when not used properly.

As a result, demand is shifting toward products that can do both, which is to deliver anti-aging benefits while repairing the skin barrier. This is where brands like Winona have gained traction, while international pharmacy brands such as La Roche-Posay and Avène still have room to better integrate anti-aging into their sensitive-skin positioning. While this raises the barrier for product development, it also creates a valuable market opportunity and strengthens potential for customer loyalty.

At the same time, the demand in the Chinese anti-aging market becomes increasingly age-specific, with a shift from purely appearance-focused concerns toward broader health and functional considerations. Consumers aged 40–49 tend to focus more on visible skin changes such as texture and firmness, while those over 50 show growing concern for cognitive function, energy levels, and physical mobility. This indicates that anti-aging is evolving from a skincare-focused category into a more holistic concept of aging management. Correspondingly, younger consumers emphasize prevention and early intervention, while older groups demand more comprehensive solutions that address both aesthetic and physiological aging, reinforcing the need for segmented and tailored product strategies.

Ingredient-focused consumption is redefining product credibility and innovation pathways

As consumer needs become more specialized, purchasing decisions are increasingly anchored in ingredient awareness rather than brand-driven marketing. In China, 72.5% of consumers prioritize ingredient composition, exceeding both efficacy claims (63.8%) and brand reputation (56.2%). This shift reflects a more informed and rational consumer base. Product credibility is evaluated through transparency, scientific backing, and perceived functionality of key ingredients.

Among these, collagen stands out as the most dominant anti-aging ingredient across categories. Its popularity is not only reflected in product claims but also in consumer awareness, with a 78.2% recognition rate in the Chinese oral anti-aging market, significantly ahead of vitamin C (74.8%) and vitamin E (68%). Notably, collagen maintains strong recognition across all age groups, positioning it as a “cross-generational” ingredient. At the same time, its application is expanding from traditional topical skincare into ingestible formats such as collagen beverages. This has become a major driver of growth in China. This shift reflects a broader trend toward internalized beauty solutions. Consumers seek to address aging from within rather than relying solely on surface-level treatments.

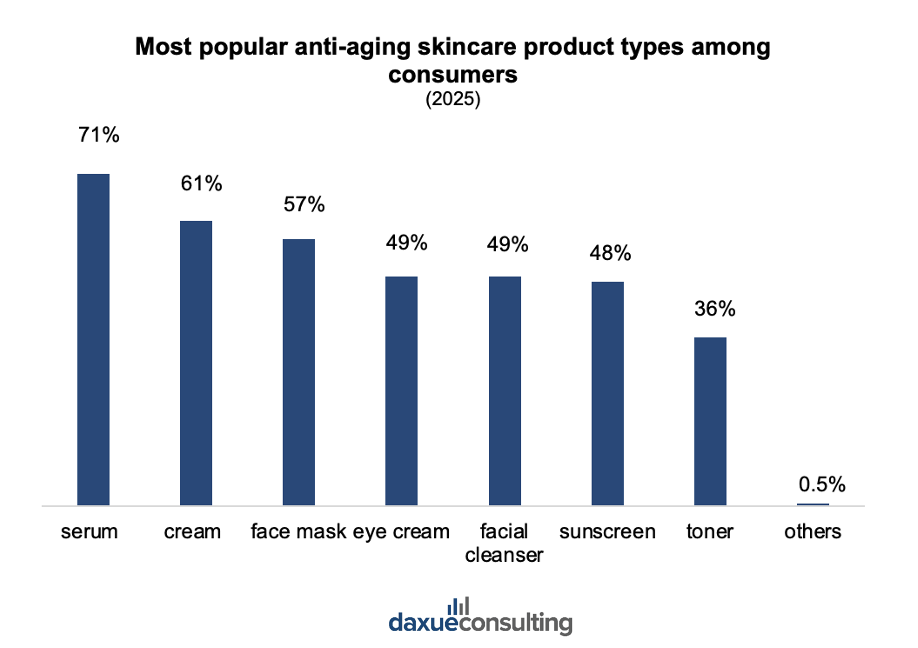

Efficacy first: Mapping consumer priorities across anti-aging categories

Consumer preferences for anti-aging skincare products show a clear concentration in efficacy-driven categories. Serums lead by a wide margin at 71%, followed by creams at 61% and face masks at 57%, indicating that consumers prioritize products perceived as delivering concentrated and visible results. Mid-tier categories such as eye creams, facial cleansers, and sunscreen cluster around 48–49%, suggesting that while these products are part of the routine, they are less directly associated with anti-aging efficacy. Toners trail behind at 36%, reflecting their positioning as supportive rather than core treatment steps.

Holistic heritage, modern anti-aging: TCM’s growing role in beauty

In parallel, the integration of Traditional Chinese Medicine (TCM) into anti-aging products is gaining traction, reflecting a preference for holistic health concepts rooted in the local cultural context. Ingredients such as ginseng, goji berries, and other herbal extracts are increasingly incorporated into formulations that combine traditional knowledge with modern clinical validation. This trend goes beyond ingredient choice. It signals a broader consumer mindset that values balance between internal health and external appearance. For foreign brands, direct adoption of TCM ingredients may not always be necessary or feasible. Yet, understanding this “holistic health and beauty” framework is critical. It shapes how consumers interpret efficacy, safety, and brand positioning, making it an important consideration for product development and market entry strategies.

Tightening regulations and the rise of domestic brands are reshaping the competitive landscape

Foreign brands in the Chinese anti-aging market face increasing regulatory and competitive pressures. On the regulatory side, authorities are strengthening oversight to curb exaggerated claims and non-compliant ingredients. Under the Cosmetics Supervision and Administration Regulation and related guidelines, anti-aging claims such as “anti-wrinkle” and “firming” must be supported by human efficacy tests, consumer trials, or credible scientific evidence. This makes it more difficult to rely on marketing-driven positioning. In the ingestible anti-aging segment, the industry is also moving toward standardized use of scientifically validated ingredients (e.g., collagen peptides, NAD+ precursors), alongside rising consumer expectations for ingredient transparency. These shifts increase compliance costs and require brands to localize both R&D and communication strategies.

At the same time, domestic brands are gaining share by leveraging stronger cultural relevance and faster market responsiveness. Brands such as Pechoin (百雀羚) have successfully combined “Eastern aesthetics” with modern marketing. Through high-visibility collaborations with major cultural events like the Spring Festival Gala, amplifying both brand recognition and emotional resonance. This reflects a broader trend where local brands are not only competing on price and product, but also on cultural identity and storytelling.

Key trends shaping the Chinese anti-aging market

- The Chinese anti-aging market is growing faster than the global average. It was driven by rising consumer acceptance and earlier adoption of anti-aging routines.

- Demand is expanding across age groups, with both the “silver economy” and younger consumers contributing to a longer and broader consumption cycle.

- Consumer needs are becoming more fragmented and specialized, shifting from general anti-aging claims to targeted solutions for specific skin concerns.

- Ingredient awareness is playing a central role in purchase decisions, with consumers prioritizing scientifically supported and transparent formulations.

- E-commerce and platform-specific dynamics are critical to market success. While regulatory pressure and the rise of domestic brands present key challenges for foreign players.