China’s fragrance market is no longer confined to the niche, luxury segment it once was, but is entering a more mature phase of development. While the perfume category continues to expand rapidly, its growth rate is expected to gradually slow from over 20% in recent years to 10.8% by 2029. At the same time, the market structure is becoming increasingly complex.

Today, China’s perfume sales are driven by both brick-and-mortar retail and online platforms, each playing distinct roles in the consumer discovery and conversion process. Physical stores offer consumers immersive fragrance experiences and showcase premium brands, while platforms such as Tmall, JD.com, and Douyin are increasingly becoming key drivers of online traffic, purchasing decisions, and competitive positioning. This diversification of platforms is reshaping the growth model of China’s fragrance market and is set to become a key feature of the market’s next phase of development.

Download our guide to Chinese gifting habits

China’s fragrance market at a glance

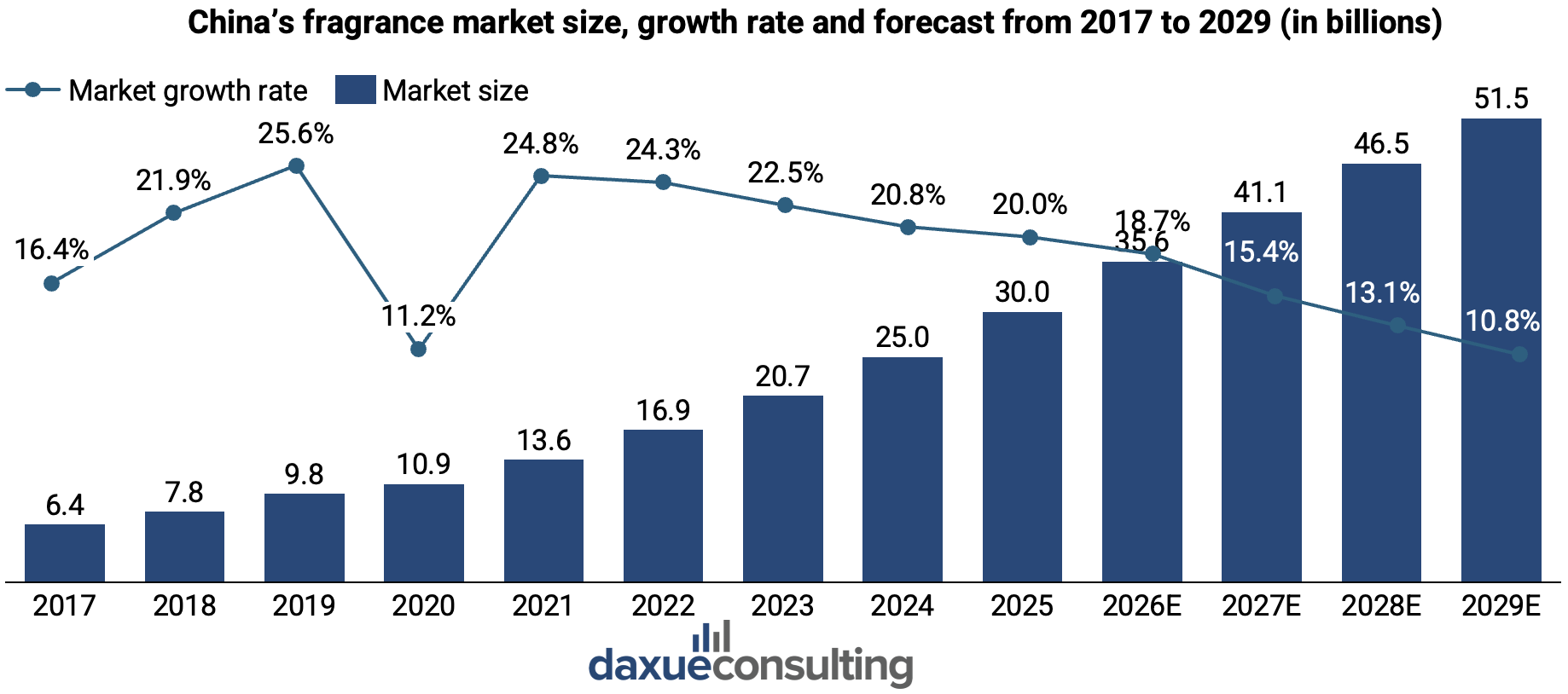

Industry reports indicate that China’s fragrance market reached RMB 25 billion in 2024, with an unadjusted market size of RMB 30 billion for 2025, a 20% increase over last year. This market has maintained a growth rate of 20% or higher for five consecutive years, demonstrating its significant market potential. It is projected to reach RMB 51.5 billion in 2029.

In terms of sales channels, both online and offline play significant roles. According to a multiple-choice survey of 1,186 consumers, when it comes to learning about and experiencing perfumes, 58.1% discover perfumes through brick-and-mortar perfume and beauty stores, indicating that physical retail environments have become a core link connecting consumers with perfume brands. These environments are also a key strategic arena for perfume brands to build brand awareness and establish a competitive edge. When it comes to actual purchases, e-commerce platforms are a major channel for perfume sales. 54.1% of consumers choose to purchase perfume on general e-commerce platforms (Tmall, JD.com), while 36.6% purchase perfume through live-streaming e-commerce platforms such as Douyin (TikTok).

Differences in user preferences for domestic and international brands across different platforms

Divergence emerges when comparing brand preferences across platforms. From January to September 2024, foreign brands accounted for 92.5% of the total merchandise volume (GMV) of perfume on Tmall. In contrast, on the Douyin e-commerce platform, the share of foreign brands dropped to 64.9%, while domestic brands accounted for 35.1%. There are multiple reasons behind this stark disparity.

First, there are significant differences in user mindset and purchasing decision-making patterns between these two platforms. Tmall has a strong utilitarian nature and operates as a search-driven, proactive shopping environment. Users typically already have brand awareness and search for “perfume” with specific needs in mind, such as brands like Dior, Chanel, or Jo Malone. Even if they do not actively search for specific brands, consumers trust that they can purchase authentic luxury goods. This is thanks to the platform’s long-established system of brand flagship stores and detailed review systems. Moreover, they are willing to spend hundreds or even thousands on imported perfumes. These users have a lengthy decision-making process and are willing to pay a premium for the brand.

The dichotomy of China’s fragrance market: Tmall vs Douyin perfume markets

Douyin, on the other hand, is a content-driven, passive discovery platform. Users often encounter perfume content by chance while scrolling. The impulse to buy stems from the video’s appeal, leading to an extremely short decision-making process. Domestic brands (such as Huazhixiao, To Summer, and Documents) are better at quickly resonating with people through visual content and emotional storytelling. Additionally, their lower price points mean there is less perceived loss associated with impulse purchases. Trust in these brands also stems primarily from influencer endorsements rather than the brands themselves.

Differences in price points and user demographics provide further insight. Among Tmall perfume buyers, there are more mature consumers who are accustomed to purchasing perfume and are familiar with imported brands. Douyin, however, reaches more new perfume users and those in lower-tier markets. This group is highly receptive to domestic brands. However, they have not yet established brand awareness of major imported labels, nor are they willing to take the risk of paying high prices in impulse-buying scenarios.

Price points and platform dynamics

When comparing the average prices of perfume brands across these two platforms, the average price on Tmall is around RMB 300, while on Douyin, it is only RMB 124. The average order value for imported perfumes generally ranges from RMB 500 to 2,000. This means that even a small number of transactions can significantly boost GMV. Although the best-selling products by sales volume are mostly high-end imported goods, the average price on the Tmall platform is driven down by many low-priced domestic and mass-market brands.

For domestic perfumes, the average order value is typically between RMB 50 and 300. Even with higher sales volumes, GMV may still be lower. The data confirms this statement. A 2024 survey of 2,275 respondents found that 50.3% considered the price range of RMB 200-500 acceptable for perfume. Meanwhile, 25.6% considered the price range of RMB 501-800 acceptable. The top ten brands by sales revenue on Tmall from January to September 2024 were all foreign brands, with Chanel ranking first at RMB 400 million. This trend continued in 2025, with Chanel maintaining its position as the top-selling brand, with sales of RMB 624 million.

Consumer demographics of China’s fragrance market

Nationwide, women remain the primary drivers of perfume consumption. In first-tier and new first-tier cities, female consumers account for up to 62.9% of the market, while in second- and third-tier cities, this proportion is slightly lower at 59.9%. Another report also notes that male consumers have become a significant consumer group, with their market share rising from 37.1% in 2023 to 40.1% in 2024. This indicates that men using perfume is no longer a niche trend. In terms of age distribution, consumers aged 26 to 35 dominate the market, accounting for 62.3% in first-tier cities and 52.4% in second-tier cities. This demographic is at the peak of their professional and social lives, possessing both the motivation and the financial means to invest in their personal image.

On what occasions do Chinese consumers use and buy perfume?

A survey shows that the top three occasions for Chinese consumers to wear perfume are dates/social gatherings, leisure travel, and major holidays. Among the main reasons for purchasing perfume, “enhance the emotional experience” ranked first at 59.7%, while “boost personal charisma in social settings” ranked second at 45.2%. New consumption trends and demands are emerging. When choosing perfumes, consumers are increasingly focusing on emotional needs and how to integrate them into their daily lives.

Growing fragrance segments in China

Beyond wearable perfumes, fragrances have found their place in various other application scenarios, including home fragrances, car fragrances, commercial fragrances, and personal care or home cleaning fragrances. Notably, the home fragrance and personal care fragrance markets have a significant reach, while the car fragrance market stands out for its rapid growth.

Home fragrances as a tool for reducing stress

Home fragrances have become more than just pleasant scents. Chinese consumers often regard them for their mood-enhancing, stress-reducing, and relaxation-promoting qualities.

Brands are diversifying their product lines with options like essential oils, candles, fireless solutions, and diffusion stones. Among these, essential oils and candles stand out as the consumer favorites. Moreover, these brands are placing a strong emphasis on sustainability, aligning with the growing demand for natural and clean ingredients.

Women drive the growth of the car fragrance industry in China

Nowadays, more women own and purchase their cars in first-tier cities. This marks a shift from men traditionally being the primary car buyers. This change is driving increased interest in the automotive fragrance industry among female consumers.

Among car fragrance categories, hanging air fresheners were the most popular products in 2021, accounting for over 60% of sales, followed by fragrant beads at nearly 20%. Liquid car fresheners and sachets made up 10% and 5% of sales, respectively.

Consumers choose car fragrances based on three key factors: the scent’s freshness and appeal, its longevity, and attractive packaging suitable for gifting. Purifying the air and eliminating odors within the vehicle is a top priority for consumers, making car fragrances an excellent choice for gifts.

5 key takeaways from China’s fragrance market

- China’s fragrance market is entering a more mature stage, as perfume expands beyond its former niche-luxury image and becomes increasingly integrated into everyday life.

- Market growth remains strong, with China’s fragrance market reaching RMB 25 billion in 2024 and RMB 30 billion in 2025.

- Physical stores remain important for discovery and brand-building, while e-commerce platforms such as Tmall, JD.com, and Douyin play a major role in driving actual purchases.

- Platform dynamics are highly differentiated: Tmall is still led by international brands and search-based shopping, while Douyin gives domestic brands stronger opportunities through content, storytelling, and lower-price impulse purchases.

- The consumer base is still led by women and the population aged 26 to 35, but rising male participation and broader adoption across city tiers suggest that fragrance use in China is becoming more mainstream.