If shopping malls in Shenzhen (深圳) are thriving and always bustling, it is because the city itself is. Shenzhen, China’s first special economic zone, established in 1980, remains one of the fastest-growing cities in the country with an average annual GDP growth rate of 5.5% (2020-2025).

It is the first-tier city with the highest annual growth rate. It is also the world’s fastest-growing wealth hub (2014-2024) with a142% increase in the number of millionaires over that period. Located in southern China, Shenzhen’s total sales of customer goods reached over RMB 1 trillion in 2023. As a key component of the retail economy, shopping malls in Shenzhen continue to expand rapidly and face ongoing innovation challenges.

Download our report on the She Economy in China

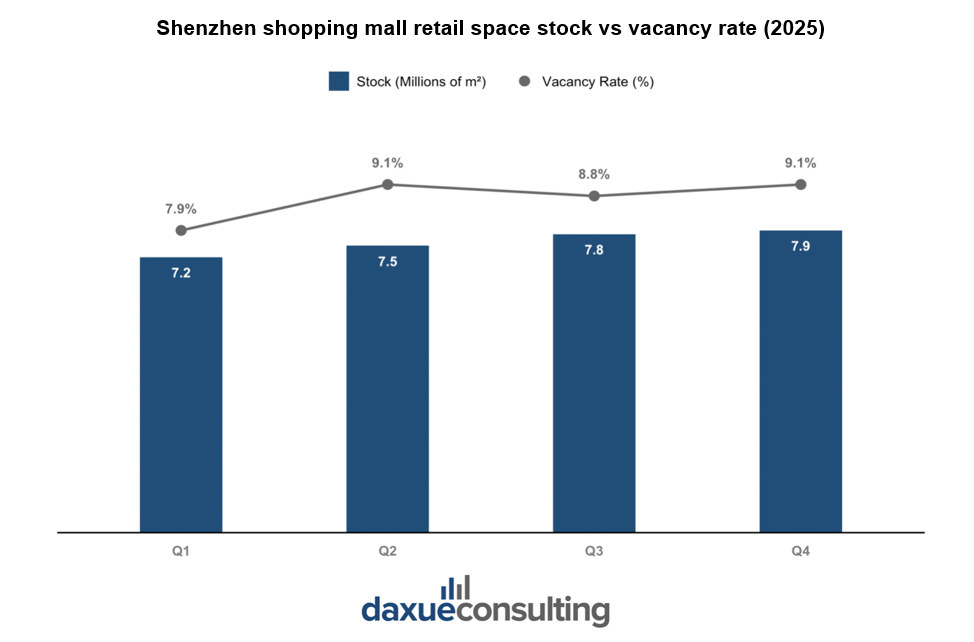

This rise in vacancy rates to 9.1% is interesting. It highlights a growing imbalance between massive supply and actual demand. This is not merely a post-pandemic adjustment, but a structural shift in the market. While new, ultra-modern centers capture attention, older, conventional shopping centers are becoming obsolete. This phenomenon of a flight to quality suggests that success no longer depends on available floor space. It was on a location’s ability to offer an experience that digital cannot replace.

Market catch-up and the high-end supply surge

Shenzhen has seen an acceleration in the construction of new high-end shopping centers with approximately 818,000 m² of new supply estimated in 2024. In Q4 2025, Shenzhen’s prime mall stock was approaching 8 million square meters with a vacancy rate of 9.1% (a slight increase from 8.6% in Q1 2024).

The city is home to dozens of major shopping malls, the largest of which are Uniworld (600,000 m²), The MixC (210,000 m²), O’Plaza (203,000 m²), and Uniwalk (with 8 floors and over 400 brands).

Unlike Shanghai and Beijing, which possess mature retail markets with established footprints, Shenzhen is currently undergoing a period of catch-up expansion. Shanghai remains the undisputed heavyweight with a total stock exceeding 26 million square meters. Meanwhile, Beijing focuses on the strategic renovation of existing spaces to maintain stability. At the same time, Shenzhen’s growth is characterized by an influx of new supply. Shenzhen stands out as the most dynamic of the three, leveraging its young demographic and increasing economic integration with Hong Kong to justify this massive physical expansion. The physical infrastructure of Shenzhen’s retail sector continued to grow steadily by about 10% over the course of the year.

Shenzhen shopping malls seek to differentiate themselves

Shenzhen’s current market dynamics are the result of a decade-long expansion. Having consistently ranked among the world’s most active markets, the city managed a massive pipeline of over 3 million square meters under construction as early as the mid-2010s. This historical momentum has established one of the largest retail footprints in China, explaining the continued pressure on vacancy rates observed in 2025.

Rapid development is not without its obstacles, as many shopping malls are struggling with homogenization (lots of them have very similar brands, which is aesthetically dull for frequent customers). This is also why newer shopping malls have stressed introducing more undiscovered brands. But diversifying brands is not enough.

The key competitive force of any shopping mall is the unique shopping experiences it provides. The design of shopping malls, clear marketing, and attractive themes will be the major determinants of unique individuality and diversification. Therefore, shopping centers are likely to engage in a battle to attract consumers’ attention, moving beyond traditional retail to differentiate themselves through unique entertainment, live performances, and high-impact events.

The new strategy for shopping malls in Shenzhen: Enhancing the aesthetics of the spaces

In recent years, Shenzhen’s retail landscape has undergone a transformation where shopping malls are no longer mere commercial hubs but also tourist destinations. Developers are looking to distinguish themselves from competing shopping centers by offering comparative advantages.

To capture the attention of consumers (and increase their dwell time), developers have shifted their focus toward retailtainment. They prioritize architectural spectacles and immersive experiences over traditional storefronts. Recent changes in average shopping time are a product of the changing design of Shenzhen’s shopping centers.

An example of this trend is UpperHills, which features a Town Village designed with vibrant aesthetics that have made it a magnet for lifestyle photography. The vibrancy of this place and the success of this photo-friendly strategy are also evident in the fact that this is where the first Muji hotel is located.

Another example is the K11 ECOAST project, which integrates museum-quality art installations directly into the consumer environment. These examples prove that in Shenzhen, the “wow factor” of the building and its cultural offerings is the main engine driving foot traffic.

The transformation of shopping malls in Shenzhen into lively public spaces

Furthermore, to stay competitive, developers have increasingly integrated expansive leisure zones that reposition shopping centers as multi-functional social hubs rather than simple retail points. These spaces are designed to encourage slow life consumption and provide visitors with areas to linger, exercise, and socialize without the pressure to purchase. An example is the Shenzhen Bay MixC, which features the Bay Garden (a green space that hosts art exhibitions and outdoor yoga sessions).

By prioritizing these non-commercial zones, Shenzhen’s malls have transformed into community lifestyle centers. Entertainment and wellness became a core reason for the shopping mall visit. This shift toward leisure-centric design represents a reimagining of retail architecture. This moves away from the traditional efficiency-first model to a dwell-time one.

This strategy operates on the idea that by de-pressurizing the environment and providing high-value experiences. As such, developers can capture a larger share of a consumer’s daily life cycle. This creates more touchpoints for spontaneous consumption and sensory engagement that online platforms simply cannot replicate.

Gen Z’s preference for community-driven spaces

This shift resonates deeply with Gen Z’s preference for “third space” over traditional malls (this strategy has already been adopted by some companies in China). A “third space” is a social environment, separate from the home (first space) and the workplace (second space), where individuals can relax, socialize, and build community in a neutral, informal setting. Industry leaders have already successfully pivoted to this model.

For instance, K11 Group has redefined the retail landscape with its Museum-Retail concept. The blend of high-end art exhibitions with shopping drives prolonged engagement. Similarly, MixC has evolved into comprehensive urban hubs that prioritize open-air layouts and social plazas. By embedding cultural and social value into the physical space, these companies have moved beyond transactional retail to become essential pillars of the modern consumer’s daily routine.

As digital storefronts and social commerce platforms (like Douyin and Xiaohongshu) become the primary touchpoints for daily consumption, certain traditional shopping centers are struggling to maintain foot traffic. The rising influence of online shopping, fueled by fast delivery services and aggressive live-streaming sales tactics, has commoditized many product categories, leading to noticeable pressure on mid-range malls.

Shenzhen’s shopping malls are a preview of the future shopping malls in China

As China’s Silicon Valley, Shenzhen serves as a testing ground where shopping malls act as the primary venues for trialing cutting-edge retail technology that could later be rolled out to shopping malls in other Chinese cities. These commercial spaces are the first to normalize innovations that remain futuristic novelties in other tier-one cities, such as the integration of immersive digital architecture that transforms the physical structure of the mall itself.

This tech-first identity is cemented by the adoption of naked-eye 3D LED displays, such as the massive L-shaped screen at Coco Park in Futian. Another example would be K11 ECOAST, located in Shekou and opened in 2025, which exemplifies Shenzhen’s fusion of technology and sustainability in retail spaces. The complex employs hospital-grade air filtration systems complemented by anti-heat vegetation and “Sponge City” infrastructure for efficient water and air management. Additionally, it integrates augmented reality for immersive visitor experiences alongside mobile apps that leverage real-time data for personalized navigation and enhanced user engagement.

By the time a digital trend or an AI-driven service model reaches Beijing or Shanghai, it has usually already been refined and standardized within the high-tech corridors of a Shenzhen mall.

Enhanced shopping experiences are a major force behind the shopping complex takeover in Shenzhen. With shopping malls offering more engagement through leisure services, interactive shopping experiences, and massive brand exposure, they are quickly becoming the premier shopping destinations for Shenzhen residents.

A surge in the number of Shenzhen’s shopping malls

As a result of large construction projects across the city, Shenzhen is striving for a multi-center pattern.

The spatial distribution of main shopping centers in Shenzhen reveals an urban structure that has evolved beyond its original core in Luohu (罗湖). Historically, the retail density was concentrated in the Luohu District, which served as the gateway for cross-border consumption from Hong Kong.

This relationship with Hong Kong has matured beyond simple shopping trips. The influence of Hong Kong developers has been important for their sophisticated and high-density retail models. Also, by integrating Hong Kong’s seamless blend of commercial and transit spaces, Shenzhen has successfully decentralized its urban structure.

However, the geographic center of gravity has shifted toward Futian (福田) and Nanshan (南山). Futian now functions as the high-end institutional heart of the city. Its CBD and Huaqiang North sectors anchor a cluster of luxury and electronic retail hubs. Further west, Nanshan District has emerged as the first destination for experimental and upscale lifestyle malls.

The Northward push: Bao’an and Longhua as secondary hubs

This westward expansion is mirrored by a northward push into the “New Districts” of Bao’an (宝安) and Longhua (龙华), which act as secondary hubs. Similarly, Longhua has transitioned from a residential suburb into a major retail player. This spatial pattern demonstrates a transition from a mono-centric border-reliant model to a diversified network of high-density retail islands.

In addition to their different locations, it is worth noting that shopping centers also differ in that they aim to attract a specific demographic and price range. For instance, The MixC stands as the city’s premier luxury landmark. It focuses on high-net-worth individuals by hosting global haute couture flagships and elite jewelry brands within a sophisticated, prestige-first architectural environment.

In contrast, COCO Park in Futian targets a younger, trend-conscious urban population, positioning itself as a high-energy lifestyle hub that blends accessible mid-to-high-range fashion with a vibrant nightlife and outdoor dining scene. Meanwhile, projects like Uniworld in Longhua cater to the burgeoning middle-class family demographic, offering an expansive one-stop retail experience that prioritizes domestic mass-market brands, large-scale entertainment facilities, and value-oriented price points.

The strategic evolution of Shenzhen’s retail ecosystem

- Driven by a 5.5% GDP growth rate and a 142% surge in its millionaire population, Shenzhen is undergoing a massive catch-up phase. Prime retail stock is approaching 8 million square meters by late 2025.

- To combat market homogenization, developers are shifting toward retailtainment, prioritizing architectural spectacles, immersive art installations, and photo-friendly aesthetics to increase customer dwell time.

- Malls are being reimagined as multi-functional community hubs or public spaces, incorporating green zones and leisure areas for yoga or art, specifically designed to capture the loyalty of Gen Z consumers.

- As the nation’s Silicon Valley, Shenzhen serves as a testing ground for futuristic retail tech, including naked-eye 3D displays, Sponge City sustainability infrastructure, and AR-enhanced visitor experiences before they scale to other tier-one cities.

- The city’s retail gravity has moved from the traditional Luohu border district toward a diversified network of high-density hubs in Futian and Nanshan, with new districts like Longhua evolving into major retail players for the burgeoning middle class.